Monopolistic Competition: 8 Main Characteristics / Causes / Features

Table of Content:

- Definition of Monopolistic Competition

- Characteristics (Causes / Features) of Monopolistic Competition Market

- Deeper Understanding of Monopolistic Competition

- How Monopolistic Competition Works in Real World

- Real Examples of Monopolistic Competition in the United States, Canada, Australia, and the World

- Inefficiencies in Monopolistic Competition

- Advantages of Monopolistic Competition

- Disadvantages of Monopolistic Competition

- Monopolistic Competition vs Perfect Competition – Difference

- Monopolistic Competition and Monopoly – What is the Difference?

- How Monopolistic Competition Behave in Short Team

- How Monopolistic Competition Behave in Long Term

- How Are Monopolistic Markets Regulated?

- FAQs of Monopolistic Competition

Definition of Monopolistic Competition Market

Monopolistic competition is a market structure where many firms offer products or services that are highly similar, highly substitutable, but not identical. There is a large number of producers/sellers in a monopolistic competition market. Barriers to entry and exit are low which results in high competition in the market.

Characteristics (Causes / Features) of Monopolistic Competition Market

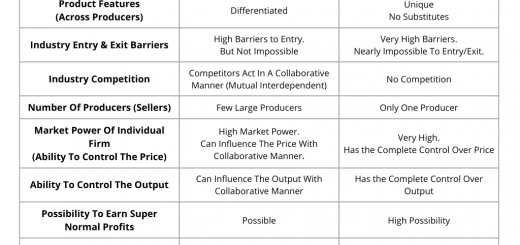

1. Products are Highly Similar, Highly Substitutable, But Not Identical

Firms that operate in a monopolistic competition market have very similar and highly substitutable products but are not identical.

Example: The shoe industry is a good example of monopolistic competition. There are many types of shoes with slightly different styles and quality levels. All these products are highly similar, highly substitutable, but not identical.

2. The Market Power of Individual Firm is Very Low (None)

An individual firm is not capable to have any significant market power. The individual firm has very low or no market power.

Example: The soap industry is classified as monopolistic competition. The market power of a single soap production firm is very low. One firm can not make any significant influence over the industry output and price.

3. A Large Number of Producers (Sellers)

There are large numbers of firms in a monopolistic competition market. Unlike monopoly or oligopoly markets, consumers have a vast variety of choices in monopolistic competition.

Example: As an example, take the clothing retail industry in the united states. There are many clothing retailers including TJX, Nike, Gap, Nordstrom, Ross Stores, Timberland, and Calvin Klein. There are many companies in the market and customers have a variety of options to choose from.

4. Barriers to Entry & Exit Are Low

New entrants can enter easily as the barriers to entry is very low. The initial investment, regulatory terms, patent restrictions, and risk factors are very low. Many new corporates can and willing to compete in the market.

Example: The soap industry is a classical example. This is an industry with a monopolistic competition where many competitors are available and entry barriers are low. Anyone can start soap manufacturing without having high barriers to entry.

5. Competition is High

Since there are very less barriers to entry, the monopolistic competition market has many rivels. The industry competition is high. This makes one or a couple of firms take entire control of the market.

Example: Hair salon is a business that is a classic example of monopolistic competition. According to ibisworld.com there are 904,718 Hair Salon Businesses in the US in 2022.

6. Less Possibility for Economies of Scale

It is hard for a firm to achieve economies of scale due to the competition. But if few firms merge then it is possible to reach economies of scale.

The firm can benefit from cost advantages when reaching economies of scale. There is an optimum production output level where the firm can produce with the minimum marginal cost.

7. The Individual Firm Cannot Influence the Market Output or Price

An individual firm can not influence the output or price of the market. The output and price depend on the market as a whole, not on individual firms or groups of firms.

Example: The clothing retail market is a monopolistic competition. One clothing retailer can not influence the market to control the price or output.

8. Supernormal Profits in the Short Term and Then Normal Profits in the Long Term

There is a certain possibility for a firm in monopolistic competition to make supernormal profits if they can fulfill a niche gap in the market. As an example, in the mobile phone production industry, if one company may create a new product with a unique design and technology, the firm will benefit from a supernormal profit.

But sooner the competitors will also produce similar mobile devices so that in the long term, the supernormal profit will be converted into normal profit.

Deeper Understanding of Monopolistic Competition

Monopolistic competition is a market structure where many companies sell similar but not identical products. Think of it like a bustling street market where multiple vendors are selling different types of coffee. Each vendor offers a unique blend or flavor, setting them apart from the others, even though they’re all essentially selling coffee. In this type of market, businesses have some control over their prices because their products have distinctive features that attract specific customers.

In the monopolistic competition, individual firm has a low power to control or influence the price and output. Each firm operates independently with resulting no room for a monopoly.

However, the competition remains fierce because there are many alternatives available. Unlike in perfect competition, where products are identical and prices are solely determined by supply and demand, monopolistic competition allows for a bit more creativity and differentiation among businesses. Companies invest in advertising, brand building, and improving product quality to stand out. This results in a variety of choices for consumers, promoting innovation and diversity in the market.

The difference between price and marginal cost is considered a mark-up. Monopolistic competition has a product mark-up, the price is always greater than the marginal cost. There is no mark-up in a perfect competition structure because the price is equal to marginal cost but the mark-up is available in monopolistic competition.

How Monopolistic Competition Works in Real World

Monopolistic competition operates by allowing numerous firms to offer differentiated products in the market. Imagine a neighborhood with various clothing boutiques. Each boutique sells clothing, but they distinguish themselves through unique styles, brands, and customer experiences. One boutique might focus on trendy, fast-fashion items, another on high-end designer wear, and yet another on eco-friendly, sustainable clothing. These differences enable each boutique to have some control over pricing, as loyal customers are willing to pay more for the specific style or brand they prefer.

Businesses compete not just on price but also through marketing, quality improvements, and exceptional customer service. If one boutique becomes highly successful, new boutiques may open, offering fresh takes on fashion. Conversely, if a boutique struggles to attract customers, it might need to innovate the offerings or close down.

This constant entry and exit of firms, combined with efforts to stand out through unique product offerings, creates a dynamic market environment that fosters innovation and variety for consumers.

Real Examples of Monopolistic Competition in the United States, Canada, Australia, and the World

1. Hairdressers in the USA

The service provided by the hairdressers is one of the most famous types of examples of monopolistic competition. According to ibisworld.com, there are 904,718 Hair Salons Businesses in the US. Some examples include Supercuts, Great Clips, Cost Cutters, Cookie Cutters, Fantastic Sams, Snip-its, etc.

The customer base is distributed among these large number of hairdresser companies. Each of the hairdresser companies has a slightly different type of expertise area and each one of them sells a slightly differentiated product to the customers.

2. Shoe Production Market in Canada

There are several reputed shoe producers in Canada. Some famous brands are Vessi, Casca Designs, Call It Spring, Zvelle, Matt & Nat, and John Fluevog.

The competition in the shoe market is very high. Many companies in the market produce substitutable products.

3. Fast Food Restaurants in Australia

There are many restaurants on any own in the world. In Australia, there are many restaurants including Brae, Lulu La Delizia, Attica, OTTO, Shobosho, Quay, Ester, Aubergine, and Fico.

All the restaurants offer food for the customers, which is a substitutable product. But the price offering of the restaurants depends on many factors such as the quality, location, and services. This is the product differentiation among the different restaurants.

4. Bakery Shops in America

There are certainly a lot of bakeries in all states and towns in the USA. Each one of them sells slightly differentiated products. Paradise Bakery & Cafe, Bouchon Bakery, Lost Larson, and Carissa’s The Bakery are some of the examples, but plenty more are available.

Relatively there is a very low entry barrier for setting up a new bakery shop which is one of the important characteristics of the monopolistic structure.

5. Grocery Shops in Canada

Grocery stores exist in a monopolistic competition market with low barriers to entry and a high number of rivalries. Also, an individual grocery shop has very low power to influence the market output and price. Typical examples of Grocery Shops in Canada are Atlantic Superstore, Fortinos, Nesters Market, Axep, Dominion, Bloor Street Market, Les Entrepôts Presto, and Extra Foods.

6. Fast Food Industry in the United States

There are many companies in the United States Fast Food Industry. McDonald’s, Subway, Burger King, and Pizza Hut are some players in the market. There are fewer barriers to entry for the Fast Food Market. Also, one company can not influence the fast-food output or fast-food price.

All the companies mentioned above sell fast foods which are highly similar in terms of fulfilling a customer’s need, but the products are not identical.

7. Online Electronics Retailers in the USA

There are many companies in the online electronic retail market in the USA. There are very low entry barriers to starting an online electronic retail website and store. Amazon, BestBuy, Walmart, MicroCenter, Crutchfield, and Kroger are some typical examples of these.

Inefficiencies in Monopolistic Competition

Monopolistic competition contains several in-efficiencies in the market. Following are the key inefficiencies explained in detail,

- Excess Capacity

In monopolistic competition, firms often produce below their optimal capacity. This happens because each firm has some degree of market power and faces a downward-sloping demand curve. To maximize profits, firms produce where marginal cost equals marginal revenue, which usually results in output levels lower than what would minimize average costs. This underutilization of capacity leads to higher average costs and less efficient production. - Allocative Inefficiency

In perfectly competitive markets, resources are allocated in a way that maximizes total societal welfare, where the price of goods equals the marginal cost of production. However, in monopolistic competition, firms have some pricing power and set prices above marginal cost. This results in a deadweight loss, as the price exceeds the marginal cost, leading to a reduction in consumer surplus and overall economic welfare. Consumers end up paying higher prices than they would in a perfectly competitive market, and fewer transactions occur. - Productive Inefficiency

Firms in monopolistic competition do not produce at the lowest point on their average cost curves due to excess capacity. As a result, the industry as a whole operates with higher costs than necessary, leading to productive inefficiency. Resources are not being used in the most efficient manner, resulting in wasted potential output. - Excessive Spending on Differentiation

Companies in monopolistic competition invest heavily in advertising, packaging, and other forms of differentiation to distinguish their products from those of competitors. While this can lead to innovation and variety, it can also result in excessive spending that does not necessarily contribute to actual product improvement. This spending represents an inefficiency, as resources could potentially be used more effectively elsewhere in the economy - Consumer Confusion and Choice Overload

The vast number of differentiated products can lead to consumer confusion and choice overload. While variety is beneficial, too many options can overwhelm consumers, making it difficult for them to make optimal purchasing decisions. This can result in suboptimal choices and reduced consumer satisfaction. - Short-Term Focus

Firms in monopolistic competition may focus on short-term profit maximization through frequent changes in product lines, marketing strategies, and pricing. This short-term focus can lead to inefficiencies as firms continually adjust their operations rather than investing in long-term productivity improvements and sustainable growth. - Barriers to Entry and Exit

While there are fewer barriers to entry and exit compared to monopoly or oligopoly markets, they are not completely absent. Initial costs for branding, marketing, and establishing a differentiated product can be significant. These barriers can prevent new firms from entering the market easily and lead to less competition than in a perfectly competitive market.

While monopolistic competition offers benefits such as product variety and innovation, it also brings inefficiencies in the form of excess capacity, allocative and productive inefficiencies, excessive spending on differentiation, consumer confusion, a short-term focus, and barriers to entry. These inefficiencies mean that resources are not used in the most effective way, leading to a loss in potential economic welfare.

Advantages (Pros / Benefits) of Monopolistic Competition

1. Few Barriers to Entry

Markets experiencing monopolistic competition has fewer barriers to entry. The advantage is with both consumer point of view and industry as a whole. There will be new rivalries in the market which brings a healthy situation for the industry. Also, consumers will not stagnate to few products since there are more producers available.

2. Differentiated Products and Services

Consumers will get the freedom to experience different products and services in the monopolistic competition market. When compared with a monopoly market, the number of products is high in the monopolistic competition market.

3. Uplift Innovation of the Industry

Since there is much competition in the market, firms try to do innovative things and uplift their product/service offering. This is a healthy situation for the industry as innovation will drive the industry to success.

4. A Large Number of Sellers / Producers

Since barriers to entry are low, there will be many sellers/producers who will join the market continuously. This is a very positive factor for the consumers and the industry as a whole.

5. Consumer Has More Information

Usually, there is a high level of advertising in monopolistic competition firms. This provides a greater advantage for the consumers with information and hence, lowers search costs. This results in more informed consumers.

6. Active Business Environment

Monopolistic competition results in an active business environment. There is good competition, since or group can not dominate in the market, market share is shared between many firms. These will result in many benefits for the industry.

7. Low Price High-Quality Products

Since with the competition, firms have to lower their profit margin and provide consumers low price competitive products. Otherwise, the market share will be loosened. Also, firms have less chance to compromise the quality since consumers can move from one brand to another easily.

Disadvantages (Cons / Drawbacks) of Monopolistic Competition

1. Less Production Efficiency of Individual Firms

Monopolistic competition market disallows monopoly to be in place. There are many competitors in the market. This results in difficulty for the companies to achieve economies of scale. A company can not reach the optimum production efficiency capability due to the unavailability of economies of scale.

2. Advertising Focus More Than Product Quality

Companies focus on advertising and promotional activities to set a particular product or service as superior to competitors. The focus shifts from product improvement to advertisements. This is a disadvantage from the consumer’s point of view.

3. More Product Alternatives for Consumers

Consumers will be dissatisfied because there are many product alternatives available for them. There will be many similar products in the market and customers will be misled to choose the correct according to the expected quality.

4. Predatory Pricing

Firms that have a large investment potential can set the prices low to attempt to drive out competitors and create a monopoly. Competitors will not be able to hold if a firm set the prices low for a consecutive duration. This is known as predatory pricing.

5. Misleading Advertising

Since with the competition and substitutable products, firms will try to invest more and more in advertising. Some advertisements will be false and misleading, uplifting the product quality more than what it is, which is not a good situation from a consumer’s point of view.

6. Excess Resource Waste

Many firms compete in the market to produce similar products, using the same resources. But with the difficulty to reach economies of scale, neither firm will hit the optimum production optimization level. This will increase the resource waste in the industry as a whole.

7. Lack of Standardized Products

Since many firms pump investment into advertisements to increase sales, firms will not focus on product quality. This will bring up the question of whether firms will produce standardized products.

Further Reference:

Monopolistic Competition and Perfect Competition – What is the Difference?

Monopolistic competition and perfect competition are two types of market structures, each with distinct characteristics. In perfect competition, many firms sell identical products, meaning no single firm can influence the market price. Prices are determined solely by supply and demand, and firms are considered price takers. They must accept the market price and focus on minimizing costs to stay competitive. Since products are identical, there is no need for advertising or brand differentiation, and consumers have perfect information about the products available.

On the other hand, monopolistic competition also involves many firms, but each sells a product that is slightly different from the others. This differentiation can be based on quality, style, brand, or other features, giving each firm some control over its prices. Firms compete not just on price but also through advertising, product improvements, and customer service. This leads to a variety of choices for consumers but also results in inefficiencies like higher prices and excess production capacity. Unlike perfect competition, where firms aim for cost minimization and optimal resource allocation, monopolistic competition focuses on attracting customers through unique product offerings and marketing efforts.

Monopolistic Competition and Monopoly – What is the Difference?

Monopolistic competition and monopoly are two distinct market structures with key differences. In monopolistic competition, many firms sell products that are similar but not identical. Each firm has some control over its prices due to product differentiation, which can be based on quality, branding, or other features. Firms compete through advertising and improving their products to attract customers. This results in a variety of choices for consumers, but it also leads to inefficiencies like higher prices and excess capacity because firms do not produce at the lowest possible cost.

In contrast, a monopoly exists when a single firm dominates the entire market, selling a unique product with no close substitutes. This firm has significant control over the market price and can set higher prices because consumers have no alternative choices. Monopolies can result from factors like exclusive control over a resource, government regulation, or significant barriers to entry that prevent other firms from competing. While monopolies can lead to high profits for the firm, they often result in lower consumer welfare, higher prices, and less innovation due to the lack of competitive pressure.

How Monopolistic Competition Behave in Short Team

In the short term, firms in monopolistic competition behave in a manner similar to monopolists due to their differentiated products. Firms in monopolistic competition focus on maximizing profits by leveraging their product differentiation and market power while managing costs and engaging in non-price competition like advertising during short term. Here’s how they operate in short term,

- Price Setting – Each firm has some degree of market power and can set its prices above marginal cost. Because their products are differentiated, they do not have to accept the market price like firms in perfect competition.

- Profit Maximization – Firms will produce at the quantity where marginal cost (MC) equals marginal revenue (MR). This is the profit-maximizing output level. Since prices are set above marginal cost, firms can earn short-term economic profits.

- Demand Elasticity – The demand curve facing each firm is downward-sloping and relatively elastic. This means that while consumers have preferences for specific brands or product variations, they can still switch to substitutes if prices rise too much.

- Advertising and Marketing – Firms often invest heavily in advertising and marketing to differentiate their products and attract more customers. This spending aims to increase demand and create brand loyalty.

- Short-Term Profits and Losses – In the short run, firms can earn profits or incur losses. If a firm’s product is popular and well-differentiated, it can make significant profits. Conversely, if a firm fails to attract enough customers, it may suffer losses.

- Entry and Exit – In the short run, the number of firms in the market is fixed because new firms cannot enter or exit immediately. This means that existing firms enjoy the profits they can make without new competitors entering to drive down prices.

How Monopolistic Competition Behave in Long Term

In the long term, firms in monopolistic competition face several dynamics that influence their behavior. Monopolistic competition tends towards a state where firms earn zero economic profits, prices reflect the costs of production, and resources are allocated efficiently in the long term. However, product differentiation and non-price competition remain important strategies for firms to maintain their market share and profitability. Here’s how they operate in long term,

- Entry and Exit – Unlike in the short term, in the long run, new firms can enter the market if existing firms are making profits. Similarly, firms experiencing losses may exit the market. This entry and exit process leads to increased competition over time.

- Product Differentiation – Firms continue to differentiate their products through innovation, branding, and marketing efforts. However, as more firms enter the market, the degree of product differentiation may diminish, as competitors offer similar products to capture market share.

- Economic Profits and Losses – In the long run, economic profits attract new firms to the market, increasing competition and driving down prices. Conversely, economic losses may lead to some firms exiting the market, reducing competition and allowing remaining firms to regain profitability.

- Price and Output Adjustments – Firms in monopolistic competition adjust their prices and output levels in response to changing market conditions. As competition increases, firms may need to lower their prices to remain competitive, leading to lower profit margins.

- Efficiency and Costs – Over time, firms may seek to improve efficiency to remain competitive. This could involve streamlining production processes, reducing costs, or investing in research and development to introduce new and improved products.

- Market Equilibrium – In the long run, the industry will reach a state of equilibrium where firms are earning zero economic profits. This occurs when firms produce at the minimum point of their average total cost curves. At this point, price equals average total cost, and resources are allocated efficiently.

How Are Monopolistic Markets Regulated?

Monopolistic markets are regulated to ensure fair competition and protect consumers from abuse of market power. Following are how and the ways it is regulated,

- Antitrust Laws

Governments create and enforce antitrust laws to prevent monopolies or cartels from forming. These laws prohibit practices like price-fixing, collusion, and mergers that reduce competition. They also break up monopolies if they become too dominant in an industry. - Consumer Protection

Regulations ensure that consumers have access to information about products and services. This includes requirements for clear labeling, advertising standards, and protections against false or misleading advertising. - Price Controls

In some cases, governments may impose price controls to prevent firms from charging excessively high prices. This can help ensure that consumers can afford essential goods and services. - Regulatory Agencies

Governments may establish regulatory agencies to oversee industries with monopolistic tendencies. These agencies monitor market behavior, enforce regulations, and investigate complaints of anti-competitive behavior. - Patent and Intellectual Property Laws

Patent laws protect inventors’ rights to their inventions for a limited time, encouraging innovation. However, they also prevent monopolistic control over essential technologies by allowing others to use them after the patent expires.

FAQs of Monopolistic Competition

- What is monopolistic competition?

Monopolistic competition is a market structure characterized by many firms selling differentiated products. Each firm has some degree of market power, allowing them to set prices above marginal cost. - How does monopolistic competition differ from perfect competition?

In perfect competition, firms sell identical products and have no market power. Prices are determined solely by supply and demand. In monopolistic competition, firms sell differentiated products and have some control over prices. - What are examples of monopolistic competition?

Examples include restaurants, clothing stores, beauty products, bookstores, and grocery stores. These industries have many firms competing with differentiated products. - Why is product differentiation important in monopolistic competition?

Product differentiation allows firms to distinguish their products from competitors’ offerings, giving them some pricing power and allowing for non-price competition. - How do firms in monopolistic competition maximize profits?

Firms maximize profits by producing at the quantity where marginal cost equals marginal revenue. They also engage in non-price competition, such as advertising and product differentiation, to attract customers. - What are the inefficiencies of monopolistic competition?

Inefficiencies include excess capacity, allocative inefficiency, and productive inefficiency. Firms may also engage in excessive spending on advertising and marketing, leading to higher prices for consumers. - How does entry and exit of firms affect monopolistic competition in the long run?

In the long run, entry of new firms increases competition, driving down prices and reducing economic profits. Conversely, exit of firms may occur if firms experience losses, leading to a reduction in competition. - How are monopolistic markets regulated?

Monopolistic markets are regulated through antitrust laws, consumer protection measures, price controls, regulatory agencies, and patent and intellectual property laws to ensure fair competition and protect consumers.

Read More:

Market Structures

Monopolistic Competition

- Overview, Definition, & Features of Monopolistic Competition

- Real Examples of Monopolistic Competition (in USA, Canada, World)

- Advantages and Disadvantages of Monopolistic Competition

Monopoly Market

- Definition, Examples, and Characteristics of Monopoly Market

- Real Examples of Monopoly Market (in the USA, Canada, Australia, World)

- Important Characteristics / Causes of Monopoly Market

- Advantages and Disadvantages of Monopoly Market

Oligopoly Market

- Definition, Types, and Characteristics of Oligopoly Market

- Real Examples of Oligopoly Market (in the USA, Canada, World)

- Seven Important Characteristics of Oligopoly Market

- Advantages and Disadvantages of Oligopoly Market

Perfect Competition