Direct Cost – Definition, Explanation, Examples

Direct cost is a type of cost associated with the production of specific goods or services. The cost of any material which directly used to produce a product/service can be considered a direct cost.

Direct cost is a type of cost associated with the production of specific goods or services. The cost of any material which directly used to produce a product/service can be considered a direct cost.

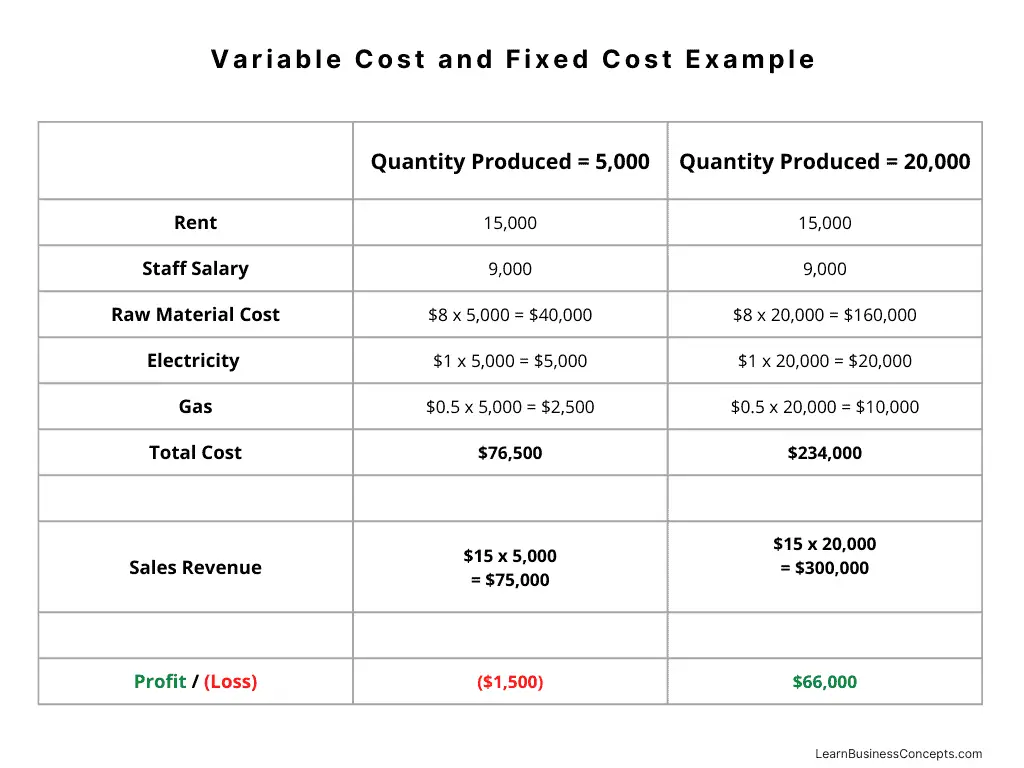

Variable costs are expenses that the amount depending on the volume of goods or services produces. In simple terms, variable cost is changing based on the production/service output quantity/volume.

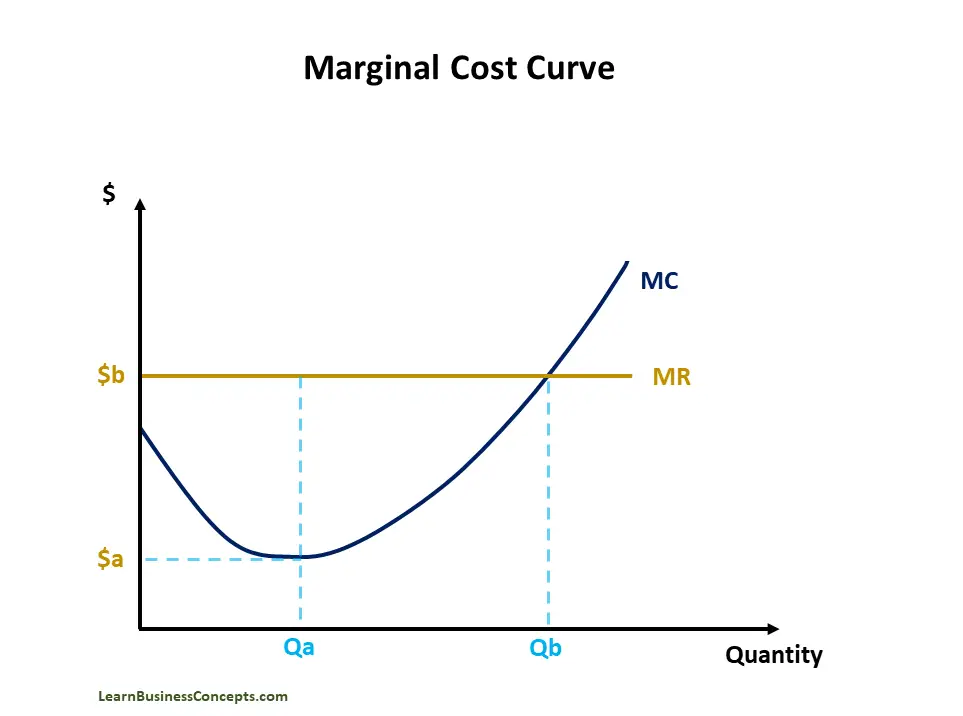

In economic terms, the marginal cost is the increase in total production cost when producing one additional unit.

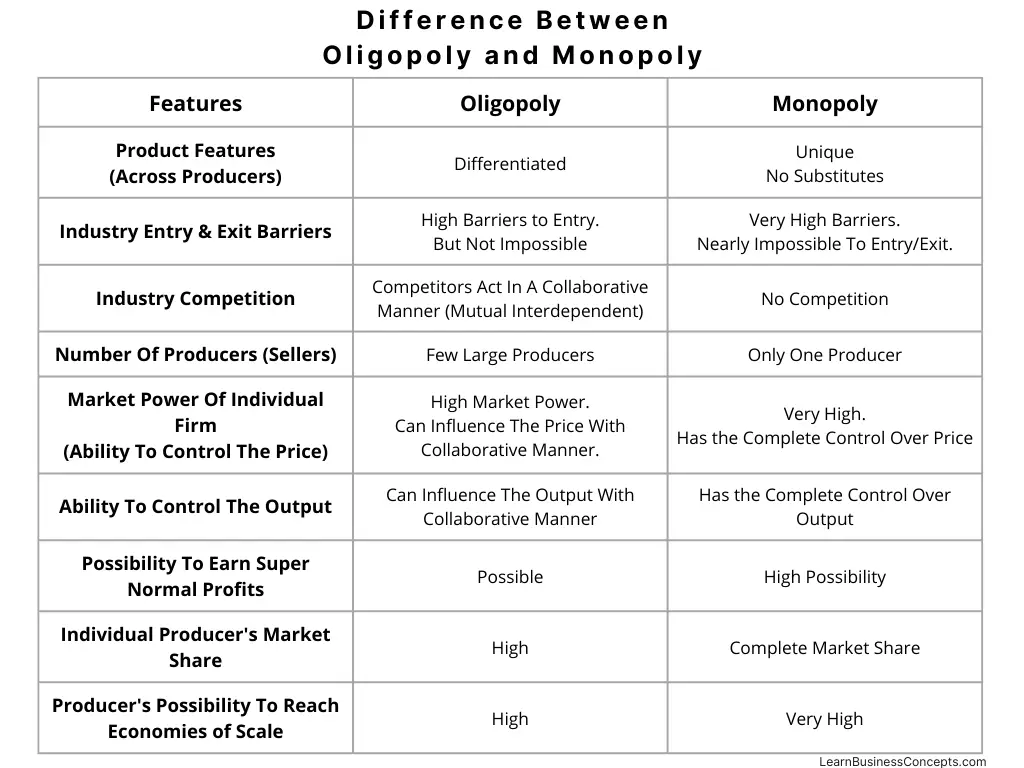

Difference Between Oligopoly and Monopoly

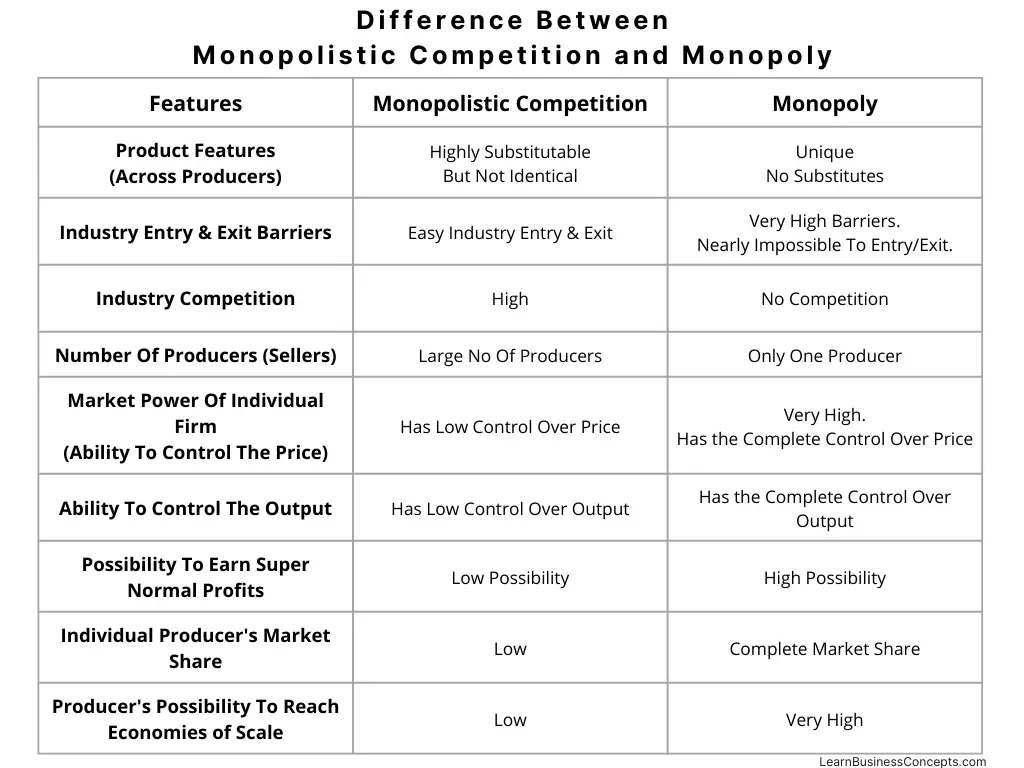

Difference Between Monopolistic Competition and Monopoly

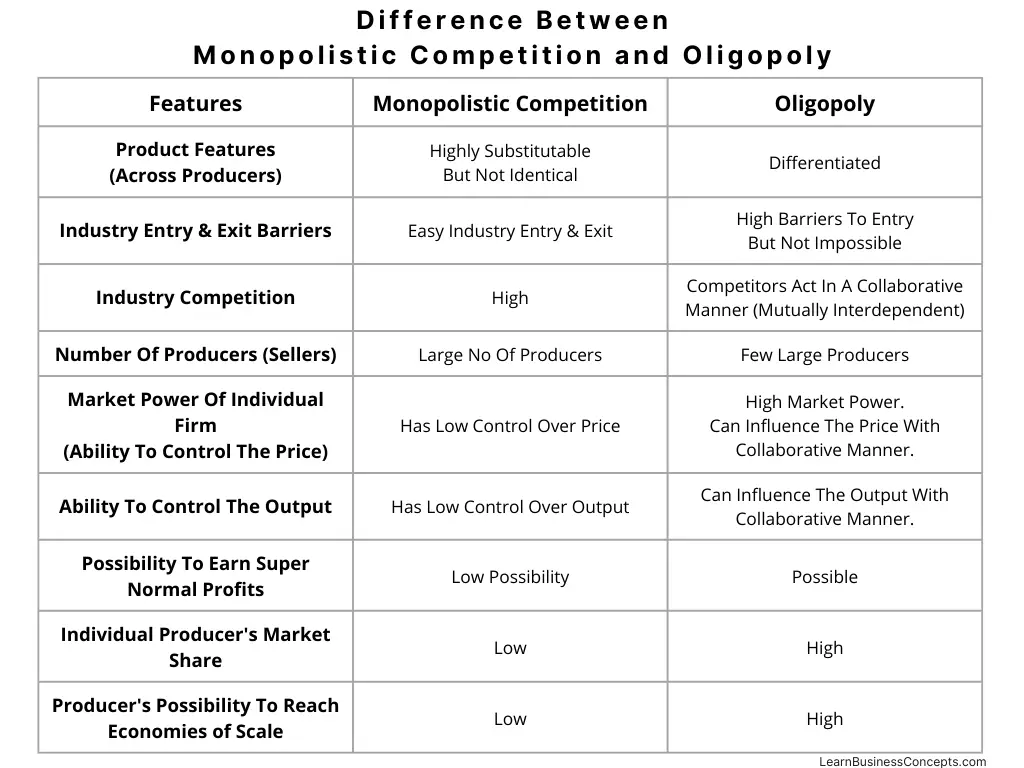

Difference Between Monopolistic Competition and Oligopoly

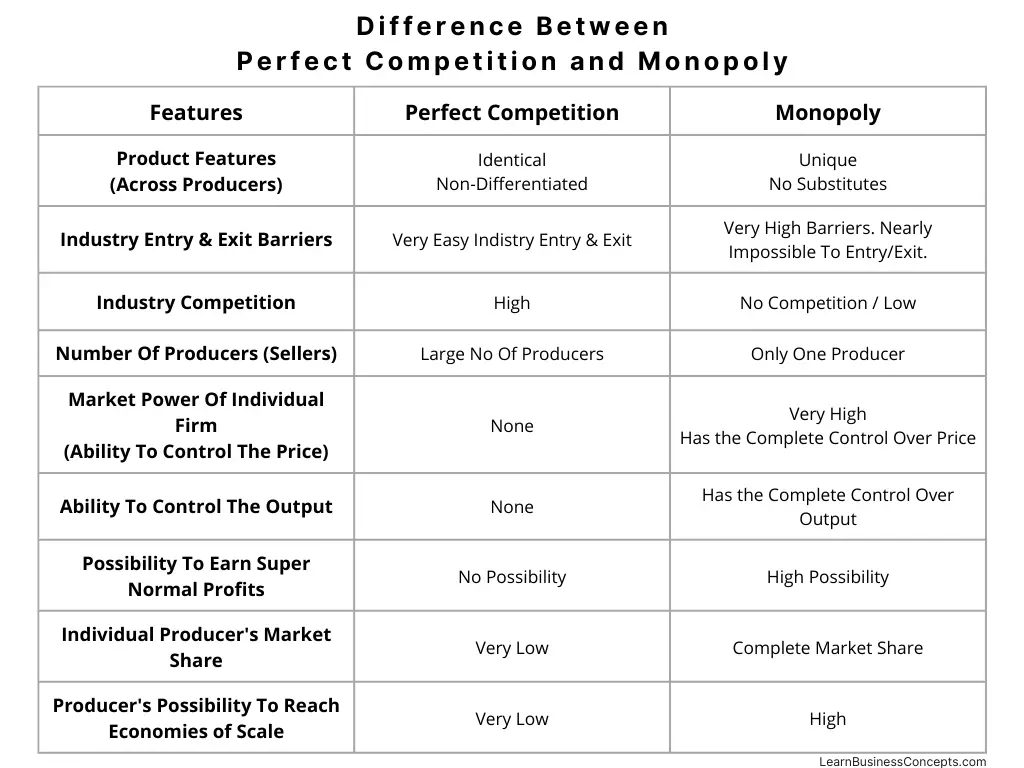

Difference Between Perfect Competition and Monopoly

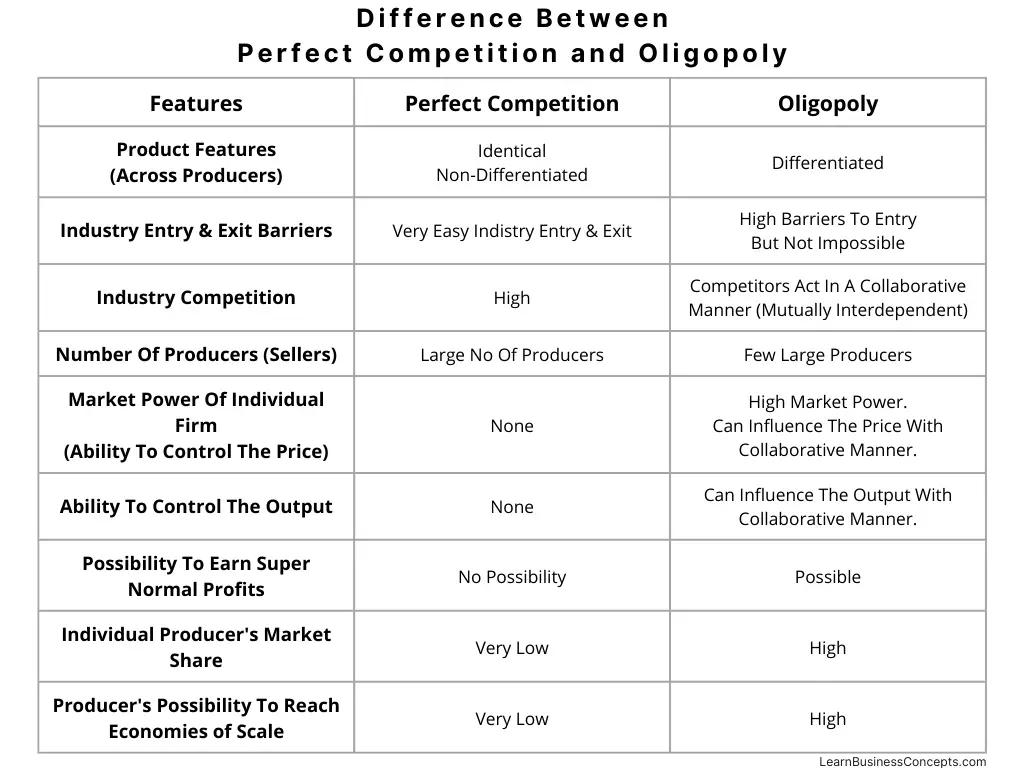

Difference Between Perfect Competition and Oligopoly

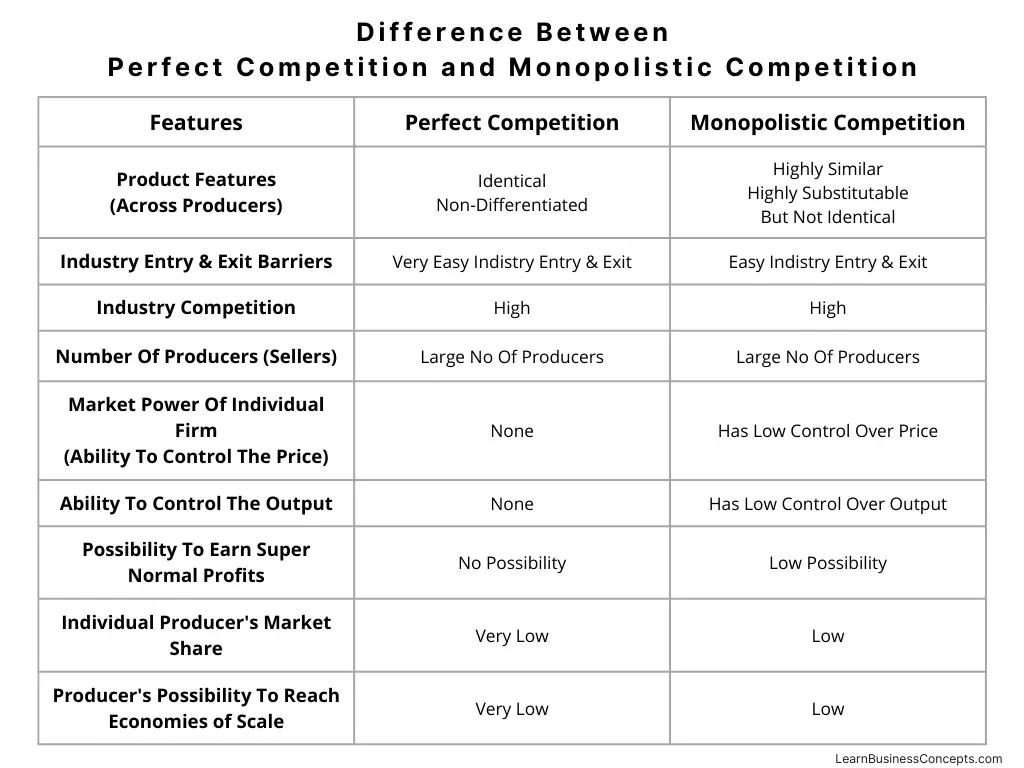

Difference Between Perfect Competition and Monopolistic Competition

Real World Examples of Perfect Competition in the United States, Canada, Australia, and Other Countries.