Indirect Cost – Definition, Explanation, Examples, Formula

Indirect costs are the costs that can not be readily determined with a specific activity but are incurred for the joint benefit of company/project activities.

Rusith Yapabandara is contributing as the key author for LearnBusinessConcepts. He has over eight years of corporate experience in multinational companies and has several years of academic consulting experience.

He is a Passed Finalist of CIMA (UK), PMP (USA) Certified, and Completed BCS HEQ (UK). He is enjoying reading, acquiring knowledge in his spare time, and also keen to share his knowledge. Rusith has been a contributor to Learn Business Concepts since 2020. You may reach him on Linkedin.

Indirect costs are the costs that can not be readily determined with a specific activity but are incurred for the joint benefit of company/project activities.

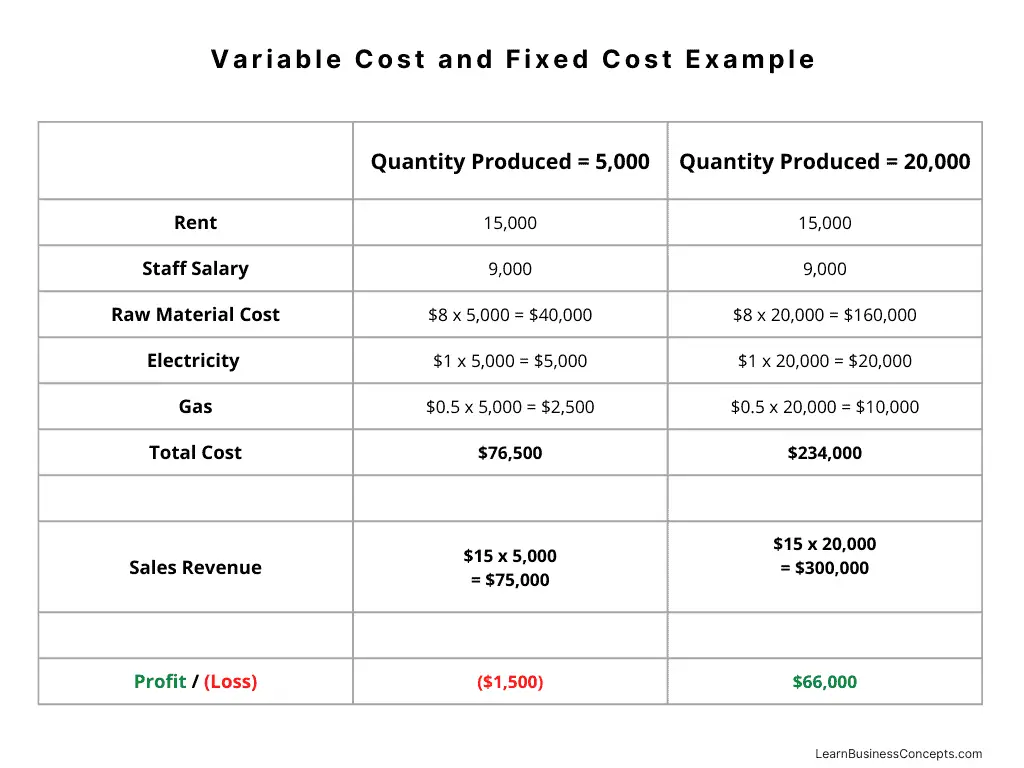

Direct cost is a type of cost associated with the production of specific goods or services. The cost of any material which directly used to produce a product/service can be considered a direct cost.

Variable costs are expenses that the amount depending on the volume of goods or services produces. In simple terms, variable cost is changing based on the production/service output quantity/volume.

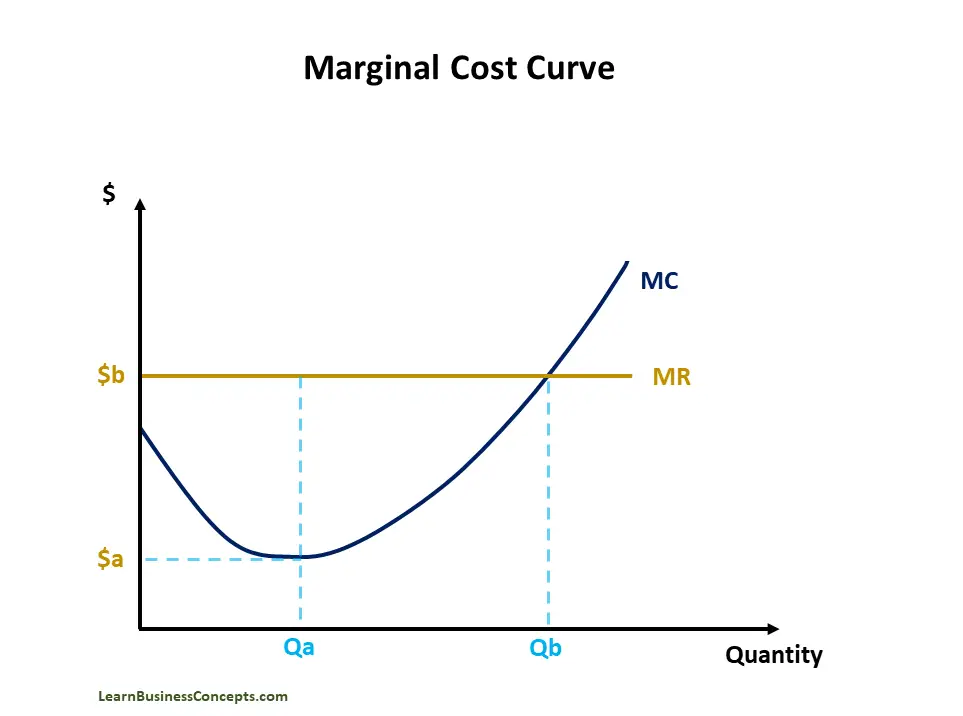

In economic terms, the marginal cost is the increase in total production cost when producing one additional unit.

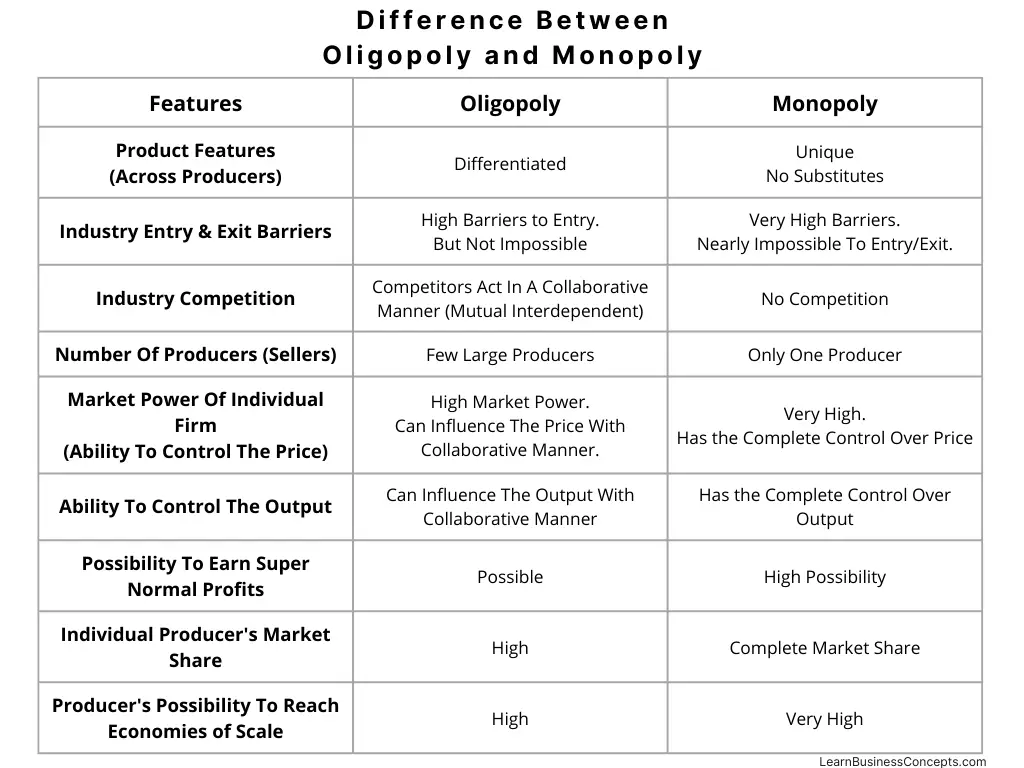

Difference Between Oligopoly and Monopoly

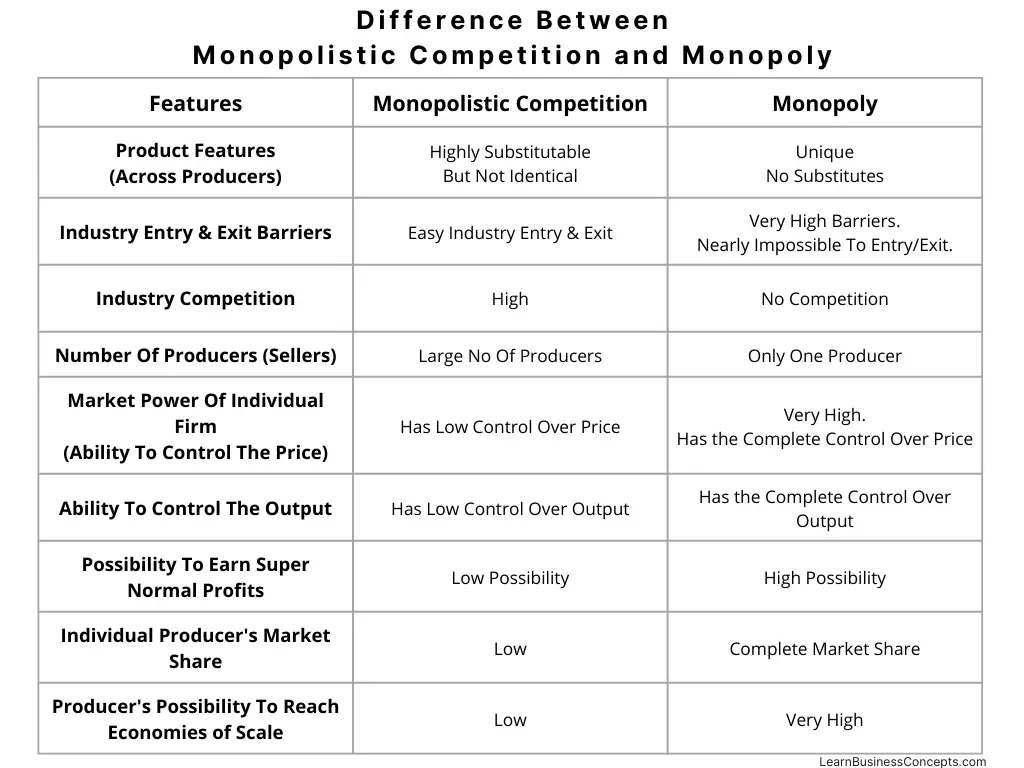

Difference Between Monopolistic Competition and Monopoly

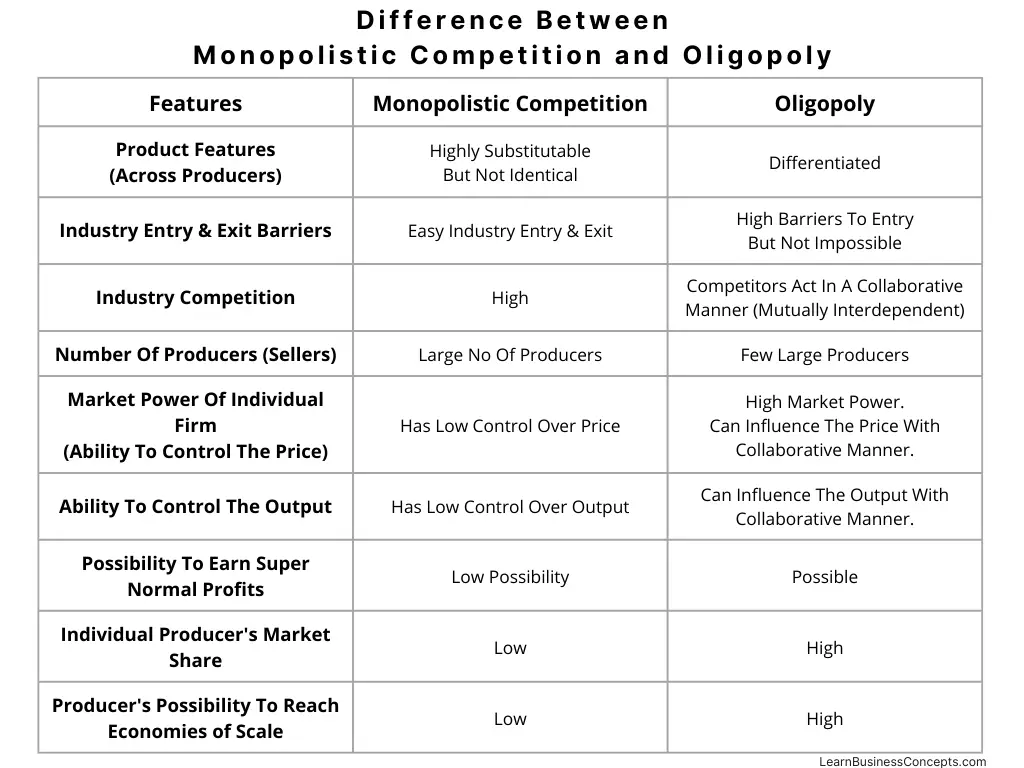

Difference Between Monopolistic Competition and Oligopoly

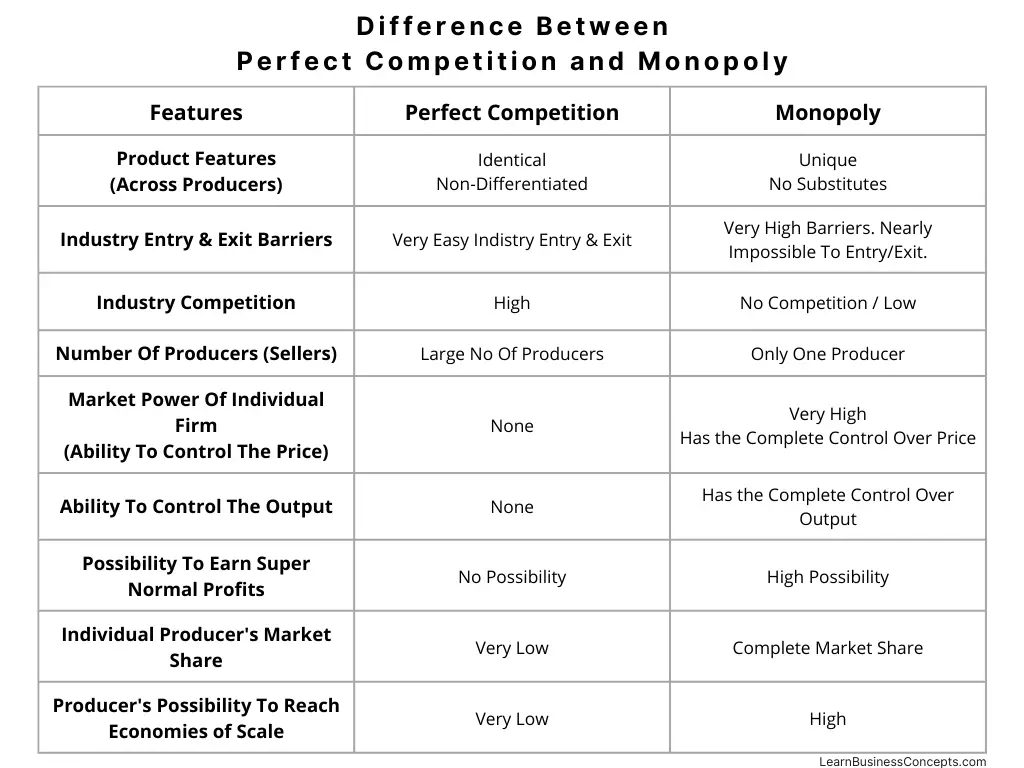

Difference Between Perfect Competition and Monopoly

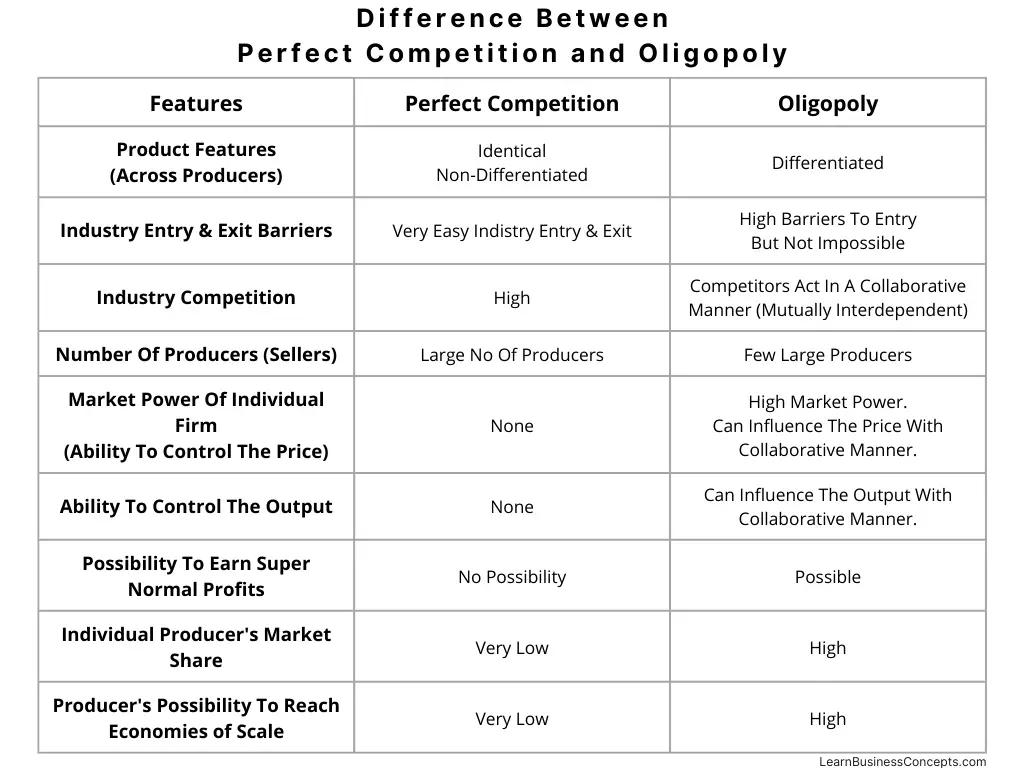

Difference Between Perfect Competition and Oligopoly

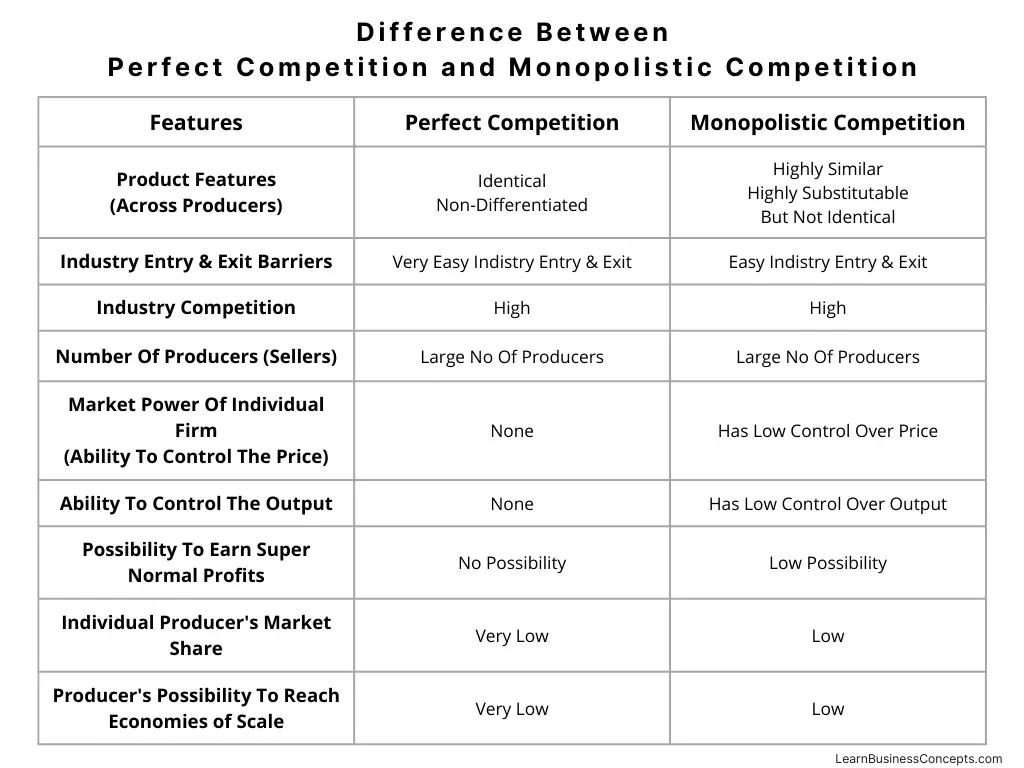

Difference Between Perfect Competition and Monopolistic Competition